Malaysia’s 8% SST in 2024 – A 2026 Retrospective for Hoteliers

Category: Hotel Management & Financial Strategy |Reading Time: 6 Minutes |Author: William

Key Takeaways :

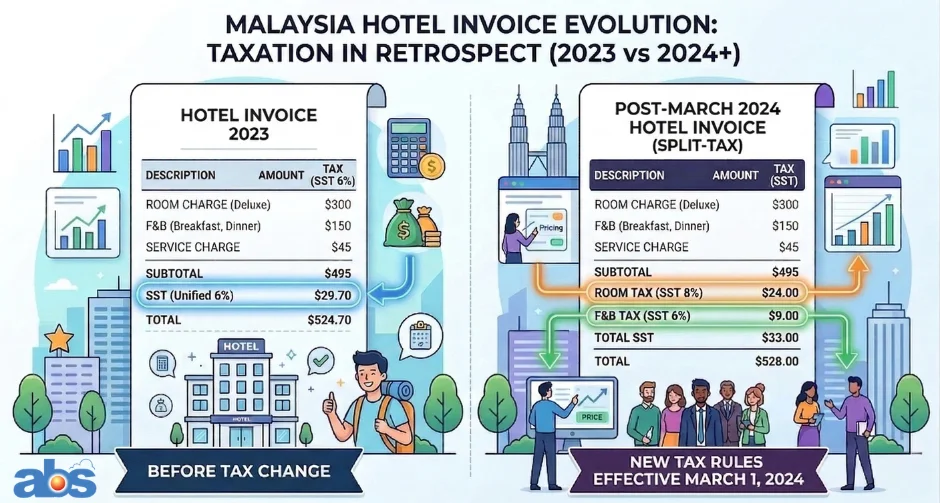

- The Shift: In March 2024, Malaysia’s Sales & Services Tax (SST) for hotel rooms increased from 6% to 8%, significantly impacting operational costs and pricing strategies.

- The F&B Exemption: Food and Beverage (F&B) services were exempt from the hike and remained at 6%, requiring hoteliers to implement split-tax invoicing.

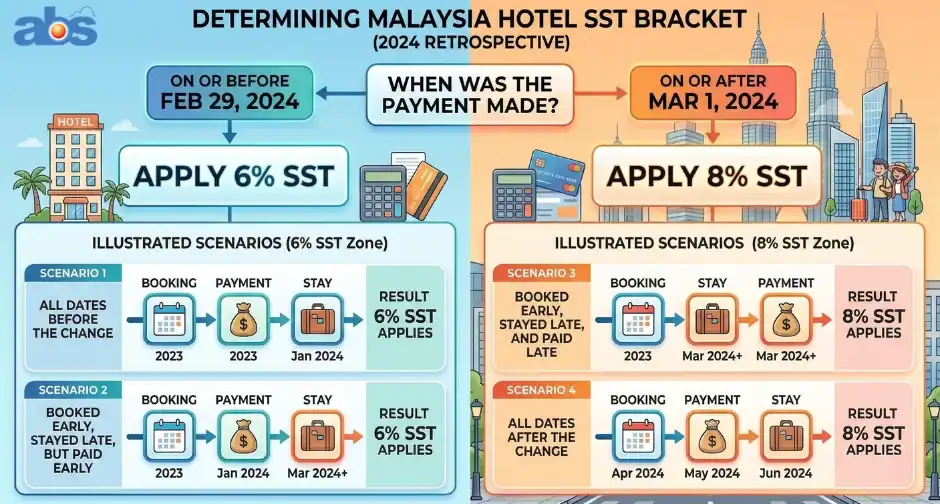

- Transition Rules: The applicable tax rate (6% vs. 8%) depended strictly on the date of payment, not the date of the hotel stay.

- System Adaptation: Hotels that succeeded updated their tax settings immediately; creating a new “8% SST” code in robust Property Management Systems (like ABS PMS) proved essential for preserving historical audit trails.

When the Malaysian government announced the Budget 2024 in Parliament, it set the stage for a significant shift in the local hospitality industry. Effective March 1, 2024, the Sales & Services Tax (SST) increased from 6% to 8%.

Now, sitting in 2026, the dust has long settled. We can clearly analyze how this change reshaped the financial landscape of the hospitality sector, the operational hurdles it introduced, and the crucial lessons hoteliers learned about adaptability and proper system management.

Understanding the Core: What Was the Malaysia 8% SST in 2024?

To understand the retrospective impact, we must first revisit the fundamentals of the tax structure. SST (Sales and Services Tax) is a consumption tax imposed on the sale of goods and specific services in Malaysia. It replaced the Goods and Services Tax (GST) in 2018 and serves as a vital revenue generator for the government.

For compliant hotel businesses, understanding exactly which goods and services fall under this umbrella has been essential for accurate reporting and remittance to the Royal Malaysian Customs Department (RMCD).

Distinguishing the Rules: F&B Exemptions

A major point of confusion during the 2024 rollout was the exemption of Food & Beverage (F&B) services from the tax hike. While room rates jumped to 8%, F&B remained at 6%. This required massive clarification for hoteliers, especially those handling hybrid invoicing for corporate events, meetings, and banquet services that combined venue rentals with catering.

Analyzing the Financial Impact of the SST Increase on Malaysian Hotels

The transition from 6% to 8% was not just a minor administrative update; it sent ripples through hotel operations, finances, and guest experiences.

The Spike in Operational Costs

Every facet of hotel management incurs costs—from maintaining pristine rooms to running welcoming lobbies. With the broader implementation of the 8% SST, supplier costs surged. Linens, towels, outsourced cleaning services, and toiletry supplies all became more expensive. Hotel management teams were forced to make a difficult choice: absorb the shrinking margins or pass the costs onto their guests.

Rethinking Hotel Pricing Strategies

Finding the “sweet spot” in pricing became a high-wire act. Set the room rate too high, and occupancy rates plummeted; keep it too low, and the bottom line suffered under the weight of the new tax. Hoteliers had to meticulously adjust room rates and service charges to offset the 2% hike while remaining competitive against neighboring properties.

The 2024 SST Rate Transition Guidelines: A Look Back

The most chaotic period for hoteliers was managing bookings made before March 1, 2024, for stays occurring after the implementation date. Based on RMCD guidelines at the time, hotels had to adhere to strict transition rules.

Important Cut-off Dates for Payments

| Payment Date | Applicable SST Rate | Rule / Condition |

| On or before Feb 29, 2024 | 6% | Applied regardless of actual check-in or check-out dates. |

| On or after March 1, 2024 | 8% | Applied regardless of when the booking was initiated. |

Managing OTA Channel Collect Payments

Following RMCD advisories, hoteliers had to apply these same payment date rules to “Channel Collect” bookings processed through Online Travel Agencies (OTAs) like Agoda or Booking.com, adding an extra layer of reconciliation to the finance department’s workload.

Survival Tactics: How Hoteliers Adapted to the 8% Sales and Services Tax

Looking back from 2026, the hoteliers who thrived were the ones who took immediate, strategic action.

System Configurations and Auditing

- Update Tax Settings: Successful hotels immediately updated their Property Management Systems (PMS), Booking Engines, and OTA extranets.

- Preserving Historical Data: Software solutions like the ABS Property Management System automated this compliance gracefully. Experts recommended adding a new tax code for “8% SST” rather than overriding the old 6% code.

Proactive Financial and Vendor Management

- Review Budgets: Management teams evaluated budgets to anticipate the effect of the SST increase.

- Explore Partnerships: Hotels collaborated with suppliers for bulk purchases to mitigate rising costs.

- Enhance Efficiency & Communicate: Properties audited energy and labor usage while maintaining transparent communication with guests regarding price adjustments.

Future-Proof Your Operations with ABS Property Management System

The 2024 SST hike taught the Malaysian hospitality industry a vital lesson: having an agile and compliant Property Management System is essential.

Ready to streamline your hotel’s tax compliance and daily operations?

Click Here to Request Demo or Contact Our Software Consultant today to see how the ABS Property Management System can simplify your accounting.

Frequently Asked Questions (FAQ) About Malaysia’s 8% Hotel SST

1. Does the 8% SST apply to hotel restaurants and catering?

No. While room rates increased to 8%, Food & Beverage services remained at 6%.

2. How should hotels handle reservations booked in 2023 but paid in 2024?

The tax rate is determined by the payment date. Payments made on or after March 1, 2024 must apply 8% SST.

3. What is the best way to update my PMS for tax changes?

Create a new tax bracket such as “SST 8%” rather than overwriting the old 6% code.

4. Are OTA bookings subject to the same transition rules?

Yes. Channel Collect payments follow the same rule: the payment date determines the applicable SST rate.